The Tax Reform is one of the most significant legislative milestones in Brazil in recent decades. But beyond its complexity and initial challenges, have you ever stopped to think about the opportunities it offers? Many tax managers and CFOs view the reform as a burden—a mountain of new rules to be deciphered and implemented. However, this perspective may be limiting the transformative potential your company can achieve.

This new tax landscape is not merely a change in tax rates or tax bases; it is a watershed moment that calls for a fundamental reassessment of how companies manage their tax obligations and, more importantly, how they use tax intelligence to drive growth. For tax managers, CFOs, business owners, and finance teams, now is the time to go beyond basic compliance and pursue strategic tax management.

In this article, we’ll explore three essential strategies that will enable your organization not only to survive but to thrive in the era of tax reform. You’ll learn how to transform your tax department from a cost center into a true driver of competitive advantage, using technology as your key ally. Get ready to demystify the complexity and discover how CAST can be your partner on this journey.

1. From Reactivity to Proactivity: Tax Planning as a Competitive Advantage

For decades, tax management in Brazil has been characterized by a reactive approach. Companies focused on complying with obligations, paying taxes, and responding to audits, constantly scrambling to keep up with changes in the law. The focus was on avoiding fines and penalties, rather than on creating value or optimizing results. This mindset, while understandable given the complexity of the Brazilian tax system, is no longer sustainable in the era of Tax Reform. According to the Federal Senate (2024), the reform brings important changes such as a 30% discount and exemption from IBS/CBS for certain sectors, which requires a proactive approach to take advantage of these benefits (Tax Reform Ensures 30% Discount and Even Exemption from IBS and CBS — Senate News).

Why the reactive mindset no longer works

The historical problem lies in the perception of the tax department as merely a cost center—an operational area that simply “pays the bills.” This perception limited the department’s strategic potential, relegating it to repetitive, low-value-added tasks. Tax reform—with the unification of taxes, the creation of the IBS and CBS, and the introduction of new regimes—exponentially increases complexity and the need for an integrated approach.

[Figure 1: Transition from Reactive to Proactive Fiscal Management]

Maintaining a reactive mindset right now means taking on high risks and missing out on valuable opportunities. A lack of foresight can lead to:

- Loss of tax benefits: Failing to identify new rules and programs in a timely manner may prevent your company from taking advantage of incentives or special programs.

- Increased costs: Business decisions made without considering the tax implications of the reform may result in a higher tax burden than necessary.

- Legal uncertainty: Delayed interpretation of new regulations increases the risk of fines and litigation.

- Waste of resources: Teams are overwhelmed by emergency adjustments instead of focusing on strategic analysis.

The Tax Reform is a game-changer. It requires companies not only to adapt, but to use this change as a catalyst to improve their processes and strategies. The impact of this change is profound, affecting everything from the pricing of products and services to cost structures and the supply chain. A practical example is the need to reassess long-term contracts and commercial agreements in light of the new rules for tax credits and the tax base for the new taxes. Those who fail to anticipate these changes may see their profit margins eroded.

The benefits of being proactive are clear:

- Identifying opportunities: Discovering new tax regimes, incentives, or structures that legally optimize the tax burden. According to the Ministry of Finance (2024), setting reference rates is a complex process that requires constant monitoring to identify the best opportunities (Ministry of Finance releases study simulating the impact on the CBS and IBS reference rates — Ministry of Finance).

- Anticipating impacts: Predicting how changes will affect cash flow, pricing, and profitability, allowing for adjustments before they become problems.

- Informed strategic decisions: Use financial data to inform decisions regarding investment, expansion, or restructuring.

- Risk mitigation: Minimizing exposure to fines and litigation, ensuring greater legal certainty.

Technology is the key enabler of this transition. Automation tools, such as the SAP Complete Tax Solution (CAST), and tax intelligence transform raw data into actionable insights, enabling your tax team to evolve from mere executors to strategists.

How to Start the Transition

The transition to proactive tax planning requires a structured approach. It is not an overnight change, but rather an ongoing process of improvement and adaptation. According to SINFRERJ (2024), the transition period for the Tax Reform extends through 2032, providing a timeframe for companies to adapt and plan their strategies (Tax Reform: Implications for Companies in 2024 and 2025 – SINFRERJ). Here are the practical steps to begin this journey:

- Comprehensive Assessment: Evaluate the impact of the tax reform on all of your company’s operations, from the purchase of raw materials to the final sale. Understand how the new taxes (IBS, CBS) and tax regimes will affect your value chain.

- Process mapping: Identify bottlenecks and inefficiencies in current tax processes. Where are there manual dependencies? Where does information not flow properly?

- Staff training: Invest in training your tax and finance team on the new rules. A well-trained team is the foundation for proactive action.

- Defining metrics: Establish tax KPIs (Key Performance Indicators) that go beyond mere compliance, measuring efficiency, optimization, and risk.

- Technology adoption: Implement solutions that automate repetitive tasks and provide tax intelligence. Tools such as Invoicecon are crucial for this transition. It enables intelligent management of electronic tax documents, ensuring automated capture, validation, and storage, freeing up your team for more complex and strategic analyses.

- Ongoing review: The tax landscape is constantly changing. Maintain a cycle of reviewing and adjusting your tax strategies, keeping pace with the regulations accompanying the tax reform.

By following these steps, your company will be building a solid foundation to turn the challenge of tax reform into a genuine competitive advantage, ensuring not only compliance but also the optimization of results.

[Figure 2: Transition Period for Tax Reform, 2024–2032]

2. Integrating Tax, Finance, and Operations: The New Standard for Efficiency

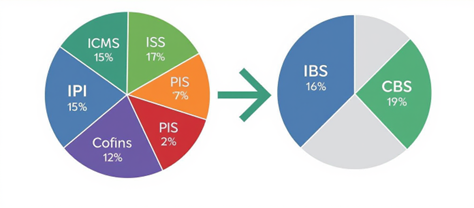

In many companies, the tax, finance, and operations departments operate as isolated silos. Each has its own systems, processes, and sometimes even jargon. This fragmentation, known as “organizational silos,” has always been an obstacle to efficiency, but with the Tax Reform, it has become a critical risk. The complexity of the new rules requires a unified vision and unprecedented collaboration among these areas. According to SINFRERJ (2024), the reform consolidates five taxes into two, which simplifies the structure but requires greater integration for accurate calculation and management.

[Figure 3: Consolidation of 5 Taxes into 2 (IBS and CBS)]

The cost of organizational silos

According to the World Bank (2020), companies in Brazil spend as much as 1,500 hours a year solely on tax compliance, a cost that is exacerbated by a lack of integration between departments. The lack of integration between tax, finance, and operations departments creates a series of problems that directly impact the company’s health and competitiveness:

- Inconsistent data: Duplicate or conflicting information across systems in different departments leads to errors, rework, and, worse still, decisions based on incorrect data.

- Operational inefficiency: Manual reconciliation and information-sharing processes take up valuable staff time that could otherwise be spent on more strategic activities.

- Audit risks: Discrepancies between tax and financial data increase a company’s vulnerability in the event of an audit. The Internal Revenue Service is increasingly seeking consistency between reported information and actual operational and financial conditions. Any inconsistency can result in assessments and heavy fines.

- Impact on decision-making: Without a 360° view, managers and executives cannot assess the tax implications of operational decisions (such as opening a new branch or launching a product) or the financial impact of tax strategies. This leads to misguided or even harmful decisions.

- Missed opportunities: A lack of integration prevents the identification of synergies and opportunities for optimization that could arise from the joint analysis of data from different areas.

The tax reform amplifies these costs. With the consolidation of taxes and the need to itemize transactions, consistency between what is recorded in the transaction, what is accounted for in the financial system, and what is reported for tax purposes is more critical than ever. An error at one end of the process can have a ripple effect throughout the entire company.

Benefits of 360° integration

Integration isn’t just about avoiding problems; it’s about creating value. When tax, finance, and operations work together cohesively, the benefits are transformative. The OECD (2023) highlights the importance of modern tax administration, which relies on the integration of data and processes to increase efficiency and compliance (The Organisation for Economic Co-operation and Development | OECD).

- Unified and strategic view: All relevant data (tax, financial, operational) converges into a single source of truth. This enables a holistic understanding of the company’s performance and the impact of decisions.

- Faster and more informed decisions: With accurate, real-time information, managers can make strategic decisions with greater confidence, assessing the fiscal and financial impact of each transaction.

- Robust, automated compliance: Automated data exchange and standardized processes ensure that tax information is always aligned with operational and financial realities, minimizing errors and the risk of penalties.

- Cost and resource optimization: Eliminating rework and identifying inefficiencies frees up staff time for higher-value activities, while also optimizing the tax burden.

- Greater agility and adaptability: In a constantly changing environment, integration enables the company to adapt more quickly to new regulations or market conditions.

A practical example is a retail company that integrates its sales (operations) systems with its financial and tax systems. When launching a promotion, the impact on revenue, cash flow, and tax burden (taking into account the new IBS and CBS) is calculated automatically and in real time. This allows the company to adjust its pricing strategy or marketing campaign even before launch, ensuring the desired profitability. On our blog, you can read about our case study: Fewer errors, greater efficiency: the role of SAP S/4HANA in logistics billing

[Figure 4: Breaking Down Silos – Integrating Tax, Finance, and Operations]

Implementing integration in your company

Implementing effective integration requires planning and the right tools. It’s not just about connecting systems, but about aligning processes and people. Here are the 6 essential steps:

- Mapping data flows: Understand how data flows (or should flow) between tax, finance, and operations. Identify the points of intersection and dependencies.

- Standardization of information: Ensure that data is recorded consistently across all areas, using the same terminology and classifications.

- Definition of responsibilities: Clarify who is responsible for each step of the process and for data integrity.

- Adoption of integrated platforms: Invest in technology solutions that facilitate communication and data exchange between departments. CAST’s solution is an example of a platform that offers this robust integration, centralizing tax and accounting management and ensuring that information flows transparently and securely between departments.

- Training and culture: Foster a culture of collaboration and train teams to use the new integrated tools and processes.

- Continuous monitoring: Track the results of the integration, identify areas for improvement, and adjust processes as needed.

By breaking down silos and promoting 360-degree integration, your company will not only be in compliance with the Tax Reform, but will also be operating at a new level of efficiency and strategic intelligence.

3. Technology as an Enabler: Compliance Without Sacrificing Efficiency

The 2024 Tax Reform presents a twofold challenge for companies: ensuring compliance with a complex set of new rules while maintaining or even increasing operational efficiency. For a long time, compliance was viewed as an unavoidable cost that often came at the expense of agility and productivity. However, modern technology offers the key to resolving this dilemma, transforming compliance into an efficient and strategic process. According to industry analysts, starting in 2026, companies will need to calculate both old and new taxes simultaneously, which requires robust technological capabilities to avoid errors and rework.

The dilemma: compliance vs. efficiency

Traditionally, the pursuit of tax compliance involved labor-intensive manual processes, complex spreadsheets, and an overreliance on human expertise. This resulted in:

High operating costs: Work hours spent on repetitive tasks, such as data entry, document verification, and form completion.

Risk of errors: Human intervention in high-volume processes increases the likelihood of errors, which can result in fines and rework.

Lack of agility: The slowness of manual processes prevents the company from responding quickly to regulatory or market changes.

Waste of talent: Qualified professionals dedicated to operational tasks rather than strategic analysis.

With the tax reform, which introduces new taxes, regimes, and ancillary obligations, this dilemma is becoming even more acute. Trying to manage this new complexity using outdated methods is a recipe for disaster. The good news is that it’s not a matter of choosing between compliance and efficiency, but rather of integrating them through automation.

Tax automation resolves this dilemma by standardizing, streamlining, and optimizing processes, ensuring that compliance is a natural byproduct of efficient operations rather than an extra and costly effort.

Tax automation: freeing up your team for strategy

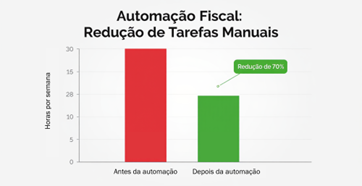

Tax automation is the backbone of modern, efficient tax management. It enables companies not only to meet their obligations but also to transform the tax function into a center of intelligence and value. The benefits are tangible and directly impact the bottom line: industry studies show that tax automation can reduce manual tasks by up to 70%, freeing up professionals who, on average, spend 28 hours a week on repetitive activities.

[Figure 5: 70% Reduction in Manual Tasks Through Automation]

- Significant time savings on manual processes: Tasks such as invoice entry, data validation, tax calculation, and tax return generation are completed in seconds, freeing up staff to focus on more complex analyses.

- Exponential increase in accuracy: Automated systems eliminate human error, ensuring that calculations and reports are always correct and compliant with the law.

- Significant risk reduction: Automation minimizes the risk of fines and penalties, as processes are standardized and auditable, with tax rules updated automatically.

- Improved decision-making: With accurate, real-time data, managers have a clear picture of the company’s financial situation, enabling them to make more informed strategic decisions.

- ROI Example: A company that automates the capture and validation of 10,000 invoices per month can save hundreds of hours of manual labor that were previously spent on verification and corrections. This time savings directly translates into lower operating costs and the ability to reallocate staff to higher-value-added activities, such as strategic tax planning.

Automation does not replace tax professionals; it empowers them, transforming them from “firefighters” into internal strategic consultants capable of identifying opportunities and proactively mitigating risks.

Key Technologies for the Tax Reform Transition

To successfully navigate the tax reform and ensure efficient compliance, your company will need robust and intelligent tools. Two solutions stand out in this context:

Soficom: A comprehensive tax and accounting management platform that integrates all information and processes. Soficom centralizes tax calculation, tax return generation, and the management of ancillary obligations, ensuring that your company is always in compliance with the latest Tax Reform regulations. Its ability to integrate with the SAP tax solution is crucial for a 360° view and for eliminating silos, promoting efficiency and data security. Learn more here.

Invoicecon: Essential for managing electronic tax documents (NF-e, NFS-e, CT-e, etc.). Invoicecon automates the capture, validation, and storage of these documents, ensuring that your company has fast and secure access to all tax information. Given the complexity of the Tax Reform, maintaining impeccable control over documents is essential for the correct crediting and calculation of new taxes. It reduces the risk of inconsistencies and optimizes the tax team’s time.

Investing in these technologies is not an expense, but a strategic investment that ensures your company’s sustainability and growth in an increasingly challenging tax environment. They serve as the bridge between the complexity of tax reform and the efficiency your company needs to stand out.

Conclusion

The Tax Reform is undoubtedly a milestone that redefines the Brazilian tax landscape. Far from being merely a challenge, it represents a unique opportunity for companies that know how to adapt and innovate. Throughout this article, we explore three essential strategies for transforming your company’s tax management, shifting from a reactive model to a proactive and strategic one. According to KPMG (2024), the reform will have profound accounting impacts, requiring a complete overhaul of companies’ systems and processes (The Accounting Impacts of Tax Reform in Brazil).

Are you ready to transform your company’s tax department into a growth engine? CAST is your ideal partner on this journey. With our proprietary solutions, we offer the tools and expertise your company needs to navigate tax reform safely, efficiently, and intelligently. We invite you to schedule a consultation with our experts to discover how we can help your company stand out. Schedule now by clicking here!

Don’t let the complexity of tax reform overshadow the opportunities. With the right strategy and technology, your company can not only adapt but also lead the way.